Indicator will only run on NT 7.0.1000.5 or later

This is a modified version of Fat Tail SessionVWAP Week V40

It has Half Deviation bands and more colour control over the individual bands

""Use at own risk as i am not a professional programmer""

Exported using NT Version 7.0.1000.8

Indicator will only run on NT 7.0.1000.5 or later

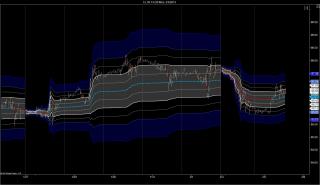

The indicator displays the Volume Weighted Average Price of the selected session. It can be used on all types of charts.

You can apply the indicators to charts with several intraday sessions. You can then select via indicator panel, for which session the VWAP shall be shown.

ETH session: The VWAP will be calculated for the full session, if ETH is selected via indicator dialogue.

RTH session: It is possible to display the VWAP for the RTH session or the night session. Set indicator to RTH and select the number of the session, for example "First" for the night session and "Second" for the RTH session.

RTH multi: The VWAP will be displayed starting from the open of the RTH session as specified and then continue through the after session.

Volatility Bands: The indicators has three different modes to calculate volatility bands. For each of the modes multipliers can be selected.

Variance_Last: The variance is calculated from the selected input values of the price bars and the last known value for the VWAP within the current session. This way of calculating the bands is similar to calculating Bollinger Bands with a variable period starting with the first bar of the session.

Variance_Distance: The variance is calculated from the selected input values of the price bars and the value for the VWAP corresponding to price. It is a variance of the vertical distance of price from VWAP. This method has two advantages. It corrects for a trend and it is much faster to calculate. It is therefore the default method of the indicator, and should always be used on high resolution charts built from ticks.

Session_Range: The quarter range of the current session is used as a measure of volatility instead of the standard deviation.

Public Holidays: For Globex instruments the indicator will display the ETH VWAP for the two-day-session including a public holiday. The indicator is preconfigured for the Globex holiday calendar. If tFriday is a holiday with trade date Monday, it will then be integrated into the following week.

Colors: Different colors can be selected for rising and falling VWAP. Also colors and opacities can be selected for the areas between the inner bands, middle bands and outer bands.

For further details on update, also see the SessionVWAP Week V40.

Update January 25, 2012: Minor enhancements. Small bug removed, which had affected the plot colors.

Category NinjaTrader 7 Indicators

|

|

|