Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,049 since Dec 2013

Thanks Given: 4,388

Thanks Received: 10,207

Little bit of forum necromancy here, trying to bring alive a five year old post.

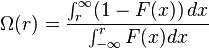

WOW. Simply WOW. I knew about Sharpe and it's problem of also penalizing good volatility and how Sortino attempts to fix that. I know about Sterling and Calmer. But I had never heard of the Omega Ratio. I'm very surprised that this thread got no responses at the time, and that futures.io has no other threads on Omega Ratio. The linked document is super interesting with explanations of the weaknesses of other methods* and how Omega includes higher moments of distributions.

The obvious issue is that other metrics (like Sortino) give you a single number, while Omega is dependent upon your desired rate of return. Portfolio A might be better than B when you want a X% return, but B is better than A when you want Y%. But is it as simple as X and Y? Aren't we generally just looking for the highest return, with the lowest risk?**

* The illustration of the flaws of a Sharpe Optimal Portfolio was excellent but the lack of an explanation of how you would construct and Omega Optimal Portfolio was disappointing!

** Haven't investigated this in anyway, but writing this I just thought maybe a ratio of two different Omega's, say the Omega of a zero return divided by the Omega of -10% return but be interesting

I can't insert links, but if you search on "calculate-the-omega-ratio-with-excel" you'll find an article about Omega ratio.

I have found the following description:

The Omega Ratio contains much more information about the return distribution, including the mean, variance, skew and kurtosis and is especially valuable for non-normal investments (such as Hedge funds, options, futures and derivatives).

Several years ago, hedge funds were subject to large losses which were in no small part due reliance on standard mean-variance optimization techniques (as pioneered by Markowitz). These approaches use mean and variance as a proxy for risk. However, this presupposes normally distributed returns; this is not the case for leveraged investments like hedge funds. Since then, the Omega Ratio and other similar approaches have grown in popularity because they favour investments with a lower probability of extreme loss.

The article also has source code as how to calculate Omega in Excel / VB.

I coded it in C++.

===

I have an automatic trading system. Part of the system evaluation are Sharpe ratio, Sortino ratio, Kelly criterium and Omega ratio.

One could calculate Sharpe ratio by hand. IMO for Sortino, Kelly and Omega manual calculations are not practical.

I find Sharpe and Sortio still valuable for a quick estimation of profitability & risk, Kelly is good for position sizing.

I use Omega to establish system profitability in respect to costs (= minimum profitability threshold). I set my minimum required profitability at 100 USD per day. An Omega of 1.0 or larger indicates I expect to cover 100 USD on costs per day. Calculation are including spread and commissions.