Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

Not sure if it matters, but on page 39 first paragraph, he says.....

I don't think it really matters in the grand scheme as to which value is chosen, as long as it is consistent as to the value chosen. But I think KNOWING that the settlement price vs. the close price will differ on the 1st of the month is useful info, particularly with regards to building an indicator around it.

The context with which MF explains, I don't know if he was making a point to differentiate between close and settle? But there is a slight difference at times.

I was asking above about the PVR, as I am creating the indicator, so I was looking for a way to be sure I am picking a consistent number going forward.

Can you help answer these questions from other members on NexusFi?

wow, so you are using the word "settle" to assume that it meant the settlement price... first... whenever he uses the settlement price, which he does in other things.. he stated it clearly... same goes for when he used the true range... I would suggest you give things another read, and read it from the perspective of someone without a clue as to what futures do... sometimes our level of "knowledge" gets on our way of learning new things.

in any event, I gave you the values to calculate todays ranges... those are from his "research" department, not made up by me.. so use those to determine see if you get the same values...

as an FYI... here is guidance from the CME on how settlement prices are determined..

well, I guess it wasnt 100% down day... but the downward bias was correct.. even if after hours we are slightly up... I wonder if we will open higher shortly...

anyhow, I closed my pos on ES at a bit of a loss on those puts, but the ZB calls paid off and covered the ES loss... i missed the second drop in the afternoon ... I need to stop paying attention to this site.. it is too damn time consuming..

BTW, from the book... the first of the month is usually statistically significant... regardless of which price one uses... so in that we agree... just that we are using settlement/first of month in a different context.. nothing to do with PVR.

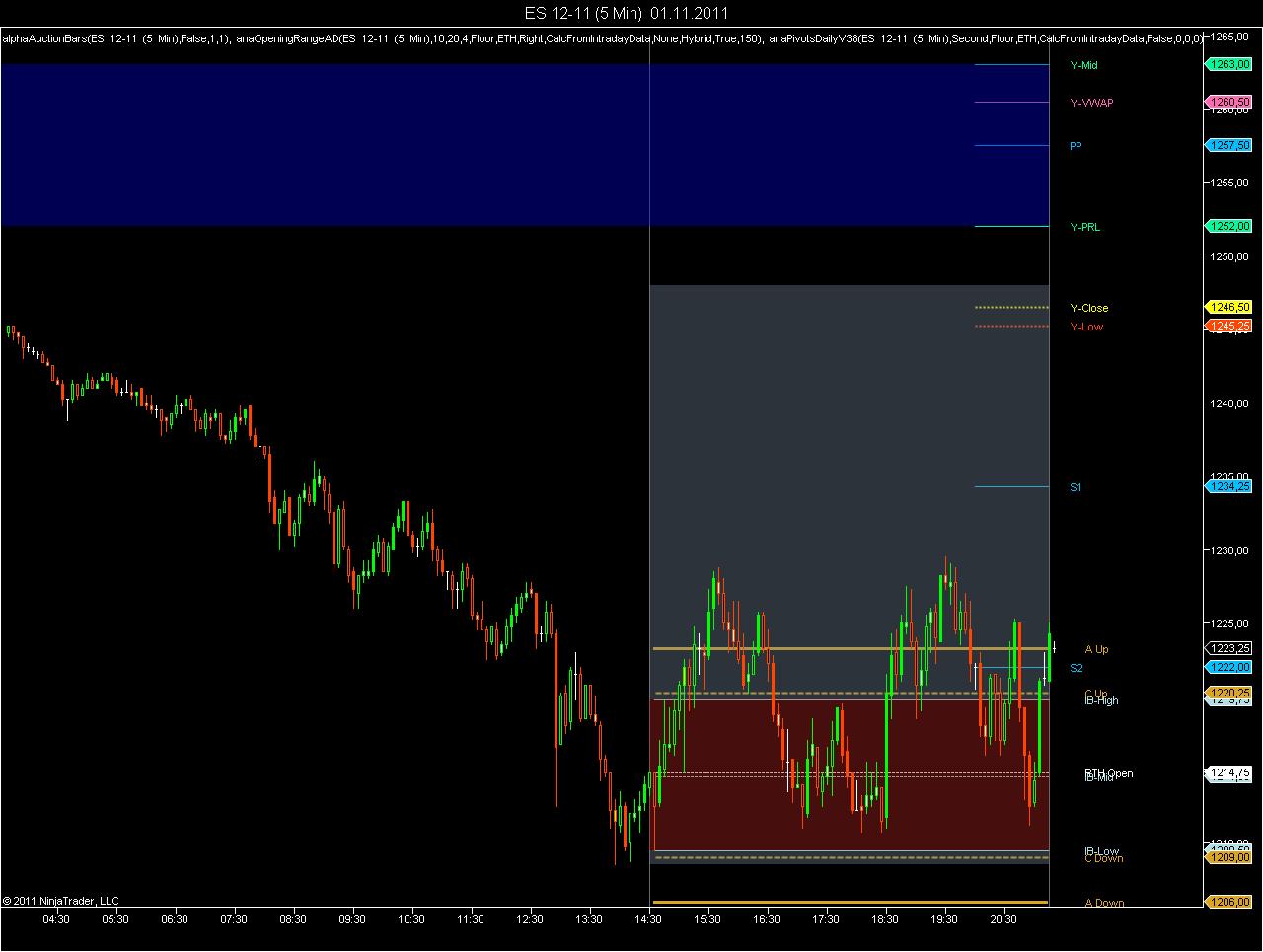

The indicator lets you choose the settlement method and you also have the choice between ETH or RTH pivots. MF has only recently switched to ETH pivots, as far as I remember he used RTH in his book.

The indicator produces exactly the same values as I can see on the sheet that you have posted. if it is set to CalculateFromIntradayData and ETH.

OH boy, participating in this thread is becoming tougher than it needs to be. I really don't know where to begin.

The point of talking about the different closing/settlement price the first of the month has nothing to do with what price does at the opening range of the year, or the month. I get your point as you are talking about another part of the book. The point is to be able to pick a value, in some CONSISTENT fashion, so that one could begin to populate various visual aids with it.

To populate these things in NT, one first has to find those values. I.e. is it done with a smaller secondary data series added to the study and assigning a look-back period to find these values with MIN/MAX() functions? Is it done simply by using something like "PriorDayHLC()," to get those values? These two questions are rhetorical btw.

As to whatever the hell MF had in mind as to which value to use, I don't know? As I mentioned earlier, I don't think it matters anyway. We are talking about a discretionary method, where the difference in a pivot zone might be off by a few tics, no two dudes are going to trade or see it the same way, so really what difference does it make? Especially given how inaccurate a way it is to measure the PVR using floor pivots. Since the point is simply to capture the 'meat of the market,' to establish a bias.

I dont see what is so difficult, unless you dont like to be opposed to things to come to the truth.. sorry, part of my nature... I guess it has to do with the culture where i work.. everything is challenged to arrived to the truth... moving on...

I agree with the basis of your statement, at the end of the day.. we are trying to find the "meat of the market"...

hmmm... where can I get the indi set to test? or is it something you are not sharing... I have all of mind done on MarketDelta.. I would share those if you guys are interested, but I dont think either of you use MD... let me know.

btw, he still uses RTH for ES today...

this is now "public" so I hurt no-one by sharing it... and you have also posted on other threads in here..