Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

2023 Bank Crisis and Meltdown: Silicon Valley Bank, Signature Bank, Credit Suisse ...

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,049 since Dec 2013

Thanks Given: 4,388

Thanks Received: 10,207

With the exception of Covid, 30yr Treasury yields have been between 2 and 3.5% for most of the last 10 years. They were borrowing at zero and lending at those rates. "Free Money"! The ridiculous thing is they could have hedged a lot of this risk but most didn't.

>>@harveys<<

> Who in their right mind would loan their money to someone for 30 years for nothing in return? <

Well, I agree with you but there is the possibility that the fund manager wouldn't have a choice because of the so called mix of capital risk investment they have to offer (risky, safe, etc). So with the government 10,20 and 30 year bonds at zero interest rates the capital is still safe ... at maturity. So an investor that waits it out will get his capital back. Will that investor get the same purchasing power at maturity - at the current rate of inflation the answer is obviously no. The faulty thinking in my view lies with the investors that wanted / wants "safe" capital at maturity and saying it doesn't matter what the markets do in the interim. I guess, they haven't thought that inflation would skyrocket but who did? The funds, banks, etc. are somewhat screwed as soon as they have the obligation to do "mark to market" such as when they have to sell.

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,049 since Dec 2013

Thanks Given: 4,388

Thanks Received: 10,207

Not an expert on this, but I gather that the Banks do not have to mark to market treasury securities that they plan to hold to maturity. I also gather that the problem at SIB & SVB was caused by the fact that due to a loss of deposits, they had to reduce assets/sell treasuries, hence realizing the loss (that they could previously hide/ignore) which then adversely effected their capital base.

A "embedded bomb"? That is no bomb that is a bond placement. No one was forced to buy these kind of papers.

As Jeffrey Gundlach said: "Put on your big boy pants and look into the mirror".

Everyone was aware of the risks they were taking at all times. Now the risks are materializing they start to cry.

Maybe they only saw the high coupon. Look at CS's 9.75% (!) Perpetual Tier 1 bond. But that is now their problem.

The magic words are: "Risk Management".

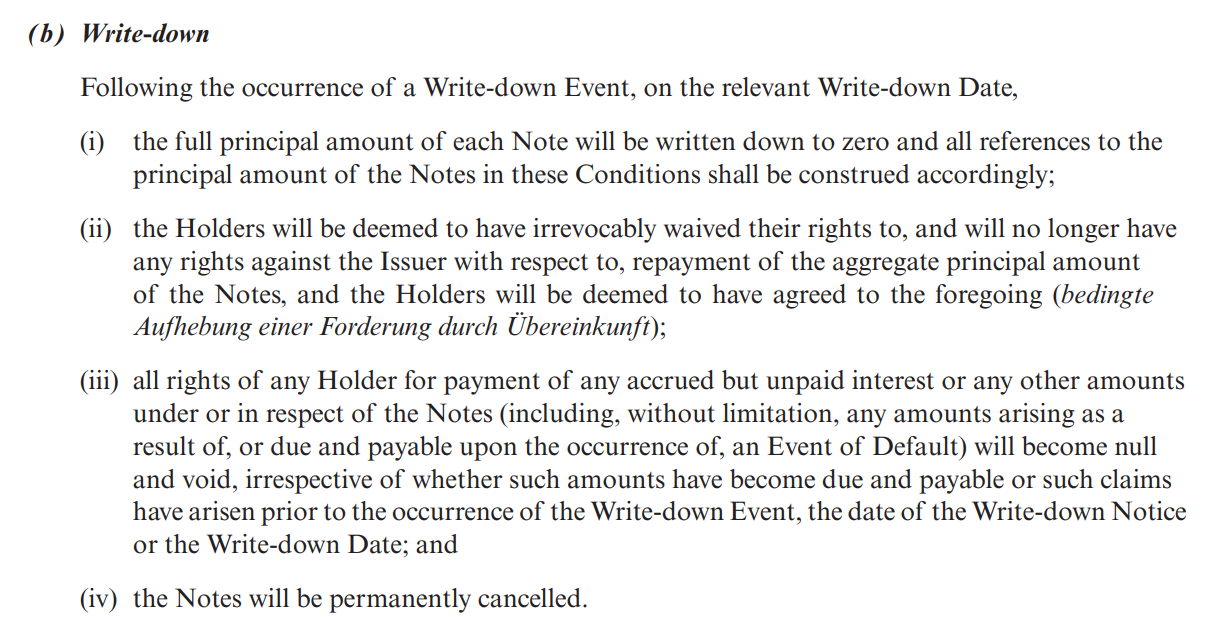

AT1 write-down bonds cleary flagged the risk of a write-down event from day one of the bonds' issuance.

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,049 since Dec 2013

Thanks Given: 4,388

Thanks Received: 10,207

@chasepatrol don't get me wrong, I'm not making excuses for anybody, I was highlighting the embedded option in the bond. 'Contingent Write-Down' is even in the Bond's Title!

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,049 since Dec 2013

Thanks Given: 4,388

Thanks Received: 10,207

From the Bloomberg Evening Briefing Email...

Pacific Investment Management and Invesco are among the largest holders of Credit Suisse�s so-called Additional Tier 1 bonds that were wiped out after the bank�s takeover by UBS. Inside Credit Suisse, things aren�t much better: The Swiss government said it�s temporarily suspending some bonus payments.

Currently the focus of a few investigations, it turns out now-deceased Silicon Valley Bank got very generous in its final months. As the lender deteriorated and regulators began detecting flaws in its risk management, SVB nevertheless opened up credit to one group: insiders. Loans to officers, directors and principal shareholders, and their related interests, more than tripled from the third quarter last year to $219 million in the final three months of 2022. That�s a record dollar amount of loans issued to insiders, going back at least two decades.