Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

(1) the time lag because the market has moved until the order is executed

(2) the bid-ask spread for market orders

(3) insufficient market depth for larger orders

(1) Decision making, order routing to broker, checking for available margin, order transmission to exchange

Prior to order execution the broker needs to check your available margin, this may take some time. HFT relies on avoiding checking for margin.

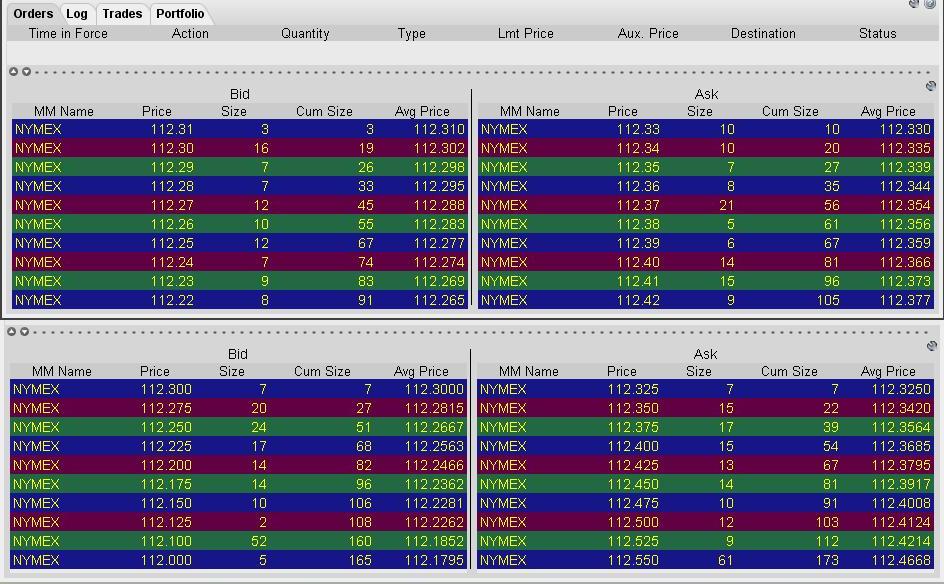

(2) The bid-ask spread for CL is typically 0.01 to 0.02 points, the bid-ask-spread for QM is typically 0.025 or 0.050 points. The snapshot below shows CL (upper panel) and QM (lower panel). The snapshot was taken at 7:30 AM EST, when market liquidity is still mediocre.

(3) The market depth for CL is considerably better than for QM, as expected. You would have to trade 2 contracts QM to make up for 1 contract CL, this would cost you additional commissions. Using data from my broker I have converted this commission to slippage, the result was about 0.01 points per half-turn.

Using the snapshot below, a market buy order would have been filled as follows

So theoretically, you would have fared better by executing part of the position (11 full contracts or 22 mini contracts) via QM and 39 contracts via CL. The average executed price would be at 112.348 against 112.352, so you would have reduced slippage by 0.004 to 0.018 points.

However, to obtain the optimal results, you would need a sophisticated algorithm, probing for market depth in real-time before executing the order. No way to benefit from this minor difference, if you execute orders manually.

So, in your estimation, do you think this sort of analysis/phenomenon would lend greater value in off hours, when the slippage is even more pronounced? I realize that the slippage is very acceptible for CL during the 7:00 a.m. hour.

I feel that if there's no direct correlation, then splitting a 4 car order when it's in very slow off hours, might reduce the overall slippage (of both orders combined).

a 4 car order in late evening can sometimes result in 4+ ticks of slippage. Compare that with a 2 car order on CL (and a 4 car order on minis) and you might find a total/aggregate slippage of less than 4 ticks. If the savings in slippage offsets or beats the increase in commission fees, then obviously, this strategy/tactic is useful for trading off hours to reduce slippage burden.

I'm also seeking to see if trading Brent with similar strategies off hours might be beneficial for reducing slippage.

For 4 cars you will definitely have no benefits splitting your order. If the slippage during off hours hurts your trading results, I would rather exclude off hours from the trading strategy.

If someone wanted to get 33 - 99 contracts filled at that moment in CL (trading hours) - do you think they would be better off rapid firing orders 11, 33 or buying the whole thing at once?

It would have to be a market order at that size in CL right?

I do not see a difference, if you fire several market orders you might get better or worse fills.

There is no answer to your question, because it is a trade-off and depends on your entry or exit strategy. If you want to make sure that you get filled (typically for exiting a position), you will use a market order, but you do not have a guaranteed price. If you want to make sure that you don't pay more than a limit price (typically for entering a position), you will use a limit order, but you do not have guaranteed fill.

It is a bit like the Heisenberg Uncertainty Principle.

I think you have to develop different trading strategy for each instrument. Even instruments that correlate don't always correlate perfectly. Trying to spread out orders to other instruments based on signal in other instrument could be problematic unless you have developed a strategy that builds that in as a signal imo. Just to purely spread out to other instruments to avoid slippage in one instrument would most likely be very inconsistent and could really skew your probabilities.

"The day I became a winning trader was the day it became boring. Daily losses no longer bother me and daily wins no longer excited me. Took years of pain and busting a few accounts before finally got my mind right. I survived the darkness within and now just chillax and let my black box do the work."

Every "strategy" has a saturation point. A point at which the positionsize becomes so large and cumbersome, that any positive gains from equity achieved on trades, is negated and washed away by adverse market impacts and commission and slippage.

Obviously this concept is easier to see/achieve when examining instruments with less liquidity or a smaller share float.

However, as I stated, if you're crafting a strategy that trades "off hours" when the market is less volitile (but also more predictable) then slippage becomes a driving force.

To illustrate my point, ask yourself.....could you trade a 1 car order during RTH for a 10 tick profit (on CL)....the answer is almost assuredly. Now ask yourself if you could trade a 100 car contract for a 10 tick move even during RTH.

The answer is....it depends. Like FT outlined, limit orders give you control over the price, but you don't have fill assurance. But in addition to price control, it also provides support/resistance (i.e. adverse market effects) so it would depend on which side you place the limit order. (i.e. if you are trading retracements and you place a limit entry order on the windward side, your order may provide a positive effect upon your strategy, as it provides resistance/support to get the trend to reverse and retrace. Contrast however, if you place the limit order on the leeward side of the trend, you may indeed be providing the wrong support/resistance to the trend retracement. You may instead be encouraging the trend to continue).

Examining the same concept (100 car order for 10 ticks) with market orders presents similar issues. Depending on the market depth, a 100 car order may cost you several ticks of "cost averaged" fill price. If it's more than 4 for the entry and more than 4 for the exit......now you're left dividing up what's left for the commission and just to break even.

These types of thoughts/analysis could be considered "cart before the horse." It's a good problem to have trading 100 cars. Conversely, if you develop a strategy and do not consider these types of issues.....you may end up coming to a dead end, where you progress no further....your strategy becomes essentially "saturated" and you either have to adjust your profit/loss amounts (which may totally change your whole strategy)

OR you could seek to find concurrent instruments that trade very similarly.

If you've spilt over into another instrument to avoid slippage burden, you're not trying to equivocate the two exactly. You acknowledge that both are independent instruments and can behave as such. However, it is advantageous to know that if Brent trades very similarly to CL, then your "system" or trading approach has a much higher chance of success than say applying it to something totally dis-similar.

I'm simply exploring options and the realm of the possible.

No one has answered my original question (although FT gave some great insights into other aspects).

WHAT IS THE UNDERLYING, PHYSICAL, REAL EQUITY COMPONENT OF A E-MINI contract? CL is obviously oil. What is the E-mini? Does an order of 2 E-Mini contracts result in a corresponding order of CL? (that is....if not a soul was trading CL and a 100 car E-mini order was initiated, would the broker then turn and issue a 50 car order for CL?) IF that's not the case, how do they run so concurrently?